Back in Sep 2015, I wrote this article outlining the investment case for SJM Holdings. The story is simple:

- the Macau gaming revenue had more than halved by Sep 2015 from a peak in early 2014 because of the corruption crackdown in China, sending Macau gaming stocks crashing more than 70% in some cases;

- the long-term fundamentals look fine, however, given that the corruption crackdown can’t go on at high intensity forever, there are major infrastructure projects connecting Hong Kong, Zhuhai and Macau that will bring more tourists, and that Macau will likely continue to remain the only place in China where gambling is legal for the foreseeable future;

- SJM’s balance sheet was pristine, with HKD 22.8 billion in cash and equivalents compared to its market capitalisation of HKD 36.5 billion (HKD 6.50 per share), and we are being paid a yield of 4% or so to wait patiently.

Back then, we had expected that

- the Macau gaming revenue will recover at some stage, from a combination of an end to the corruption crackdown and the completion of major infrastructure projects;

- SJM’s market share of around 20-23% of total Macau gaming revenue will continue dropping and then recover once the new Grand Lisboa Palace construction at Cotai is finished in late 2017.

Fast forward to May 2018, what can we say about those projections.

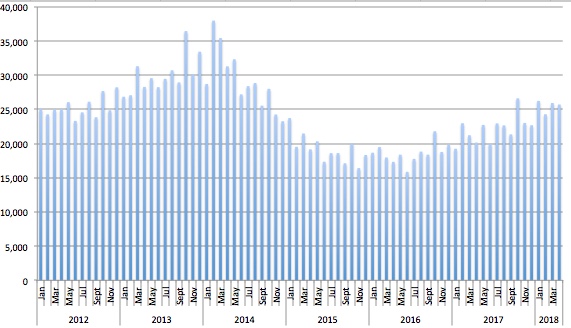

The Macau gaming revenue has certainly recovered, as shown in the following chart. In fact, Sep 2015 is pretty close to start of the bottom of the cycle.

The corruption crackdown has certainly been easing with each consolidation of power by the Chinese president, culminating in his appointment as president for life in March 2018. With the political imperative gone, I don’t expect any more corruption crackdown for at least the next few years.

The Hong Kong – Zhuhai – Macau Bridge was one year late in construction but it is expected to open on 1 July 2018. This, together with all the new casinos on the Cotai strip, should bring more Chinese tourists to Macau in the period ahead. The supply-side reform in China has also been successful in defusing the bad-debt issue in China’s financial system so a risk of a major credit event that affects consumer spending has also subsided.

So the macro outlook for Macau looks good. How did SJM perform operationally as a company in that period?

Not that well, unfortunately. SJM’s market share has fallen to 14.7% of Macau’s total casino gaming revenue during Q1 2018. Unlike its peers, it couldn’t quite reduce its expenses at the same rate as revenue declines so profits and margins have been crushed in the past 2 years. The Grand Lisboa Palace construction had a few mishaps and the new integrated resort is not expected to open until 2019, late by at least 1.5 years. SJM’s net cash position is down to HKD 8 billion, as funds go toward the construction of Grand Lisboa Palace. Finally, Stanley Ho is stepping down in June but the succession planning is messy, with two co-chairs (Angela Ho and Daisy Ho) and the current not-so-effective management largely in place.

Despite all that, the market capitalisation of SJM as of 28 May 2018 is HKD 55.2 billion, or HKD 9.75 per share. We are sitting on a 50% gain over 2.5 years (or ~12.5% pa compounded), which is not a bad outcome, after a roller-coaster ride with the stock going down to HKD 4.60 in early 2016 before recovering in mid 2017 or so.

So do we hang on or is it time to sell?

There are a few factors in the valuation equation. One is the average over-the-cycle Macau gaming revenue. The other is SJM’s expected share of that revenue. In the base case scenario, we can expect the average Macau gaming revenue to stay around the current level of 25 billion patacas per month and that SJM’s market share, after the opening of Grand Lisboa Palace, to go back to the more normal level of 20-23%. Back in H1 2012, the Macau gaming revenue was around 25 billion patacas per month, SJM’s market share was around 27%, and its share price is around HKD 12.50. The current share price of HKD 9.75 thus looks like it’s basically projecting that base-case scenario.

I think the days of 27-30% market share for SJM is gone. The upside scenario is thus entirely contingent on the average over-the-cycle Macau gaming revenue to be north of 25 billion patacas per month. This is certainly not impossible, but I suspect the actual average Macau gaming revenue to be closer to 25 billion than 35 billion patacas per month. This puts a limit to the upside to SJM’s share price at around HKD 12-14.

What about the downside? The major risk is of course that the Chinese government will decide that gambling is to be phased out completely in Macau and SJM gets allocated a smaller and smaller number of gaming tables over time, or loses its gambling license completely. This is a real if small possibility.

On the balance of things, pulling chips off this winning position as it goes to HKD 11-12 is probably the right thing to do here, especially if this is becoming a significant position in one’s overall portfolio.