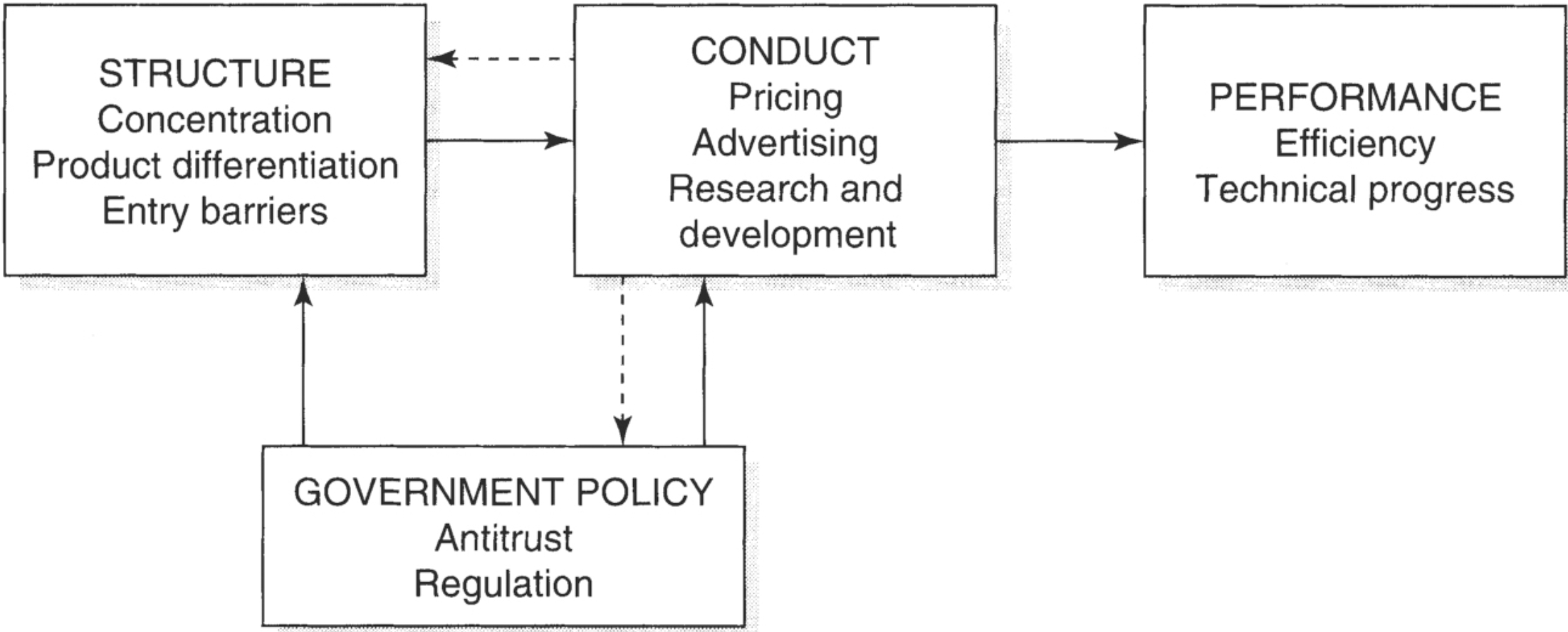

Modern competitive analysis started in the 1930’s with the introduction of the Structural-Conduct-Performance (SCP) paradigm (shown in Figure 1 below) that was used to analyse the causal dynamics of Industrial Organisation, the field of study concerned to a large extent with how public policy can limit monopoly power.

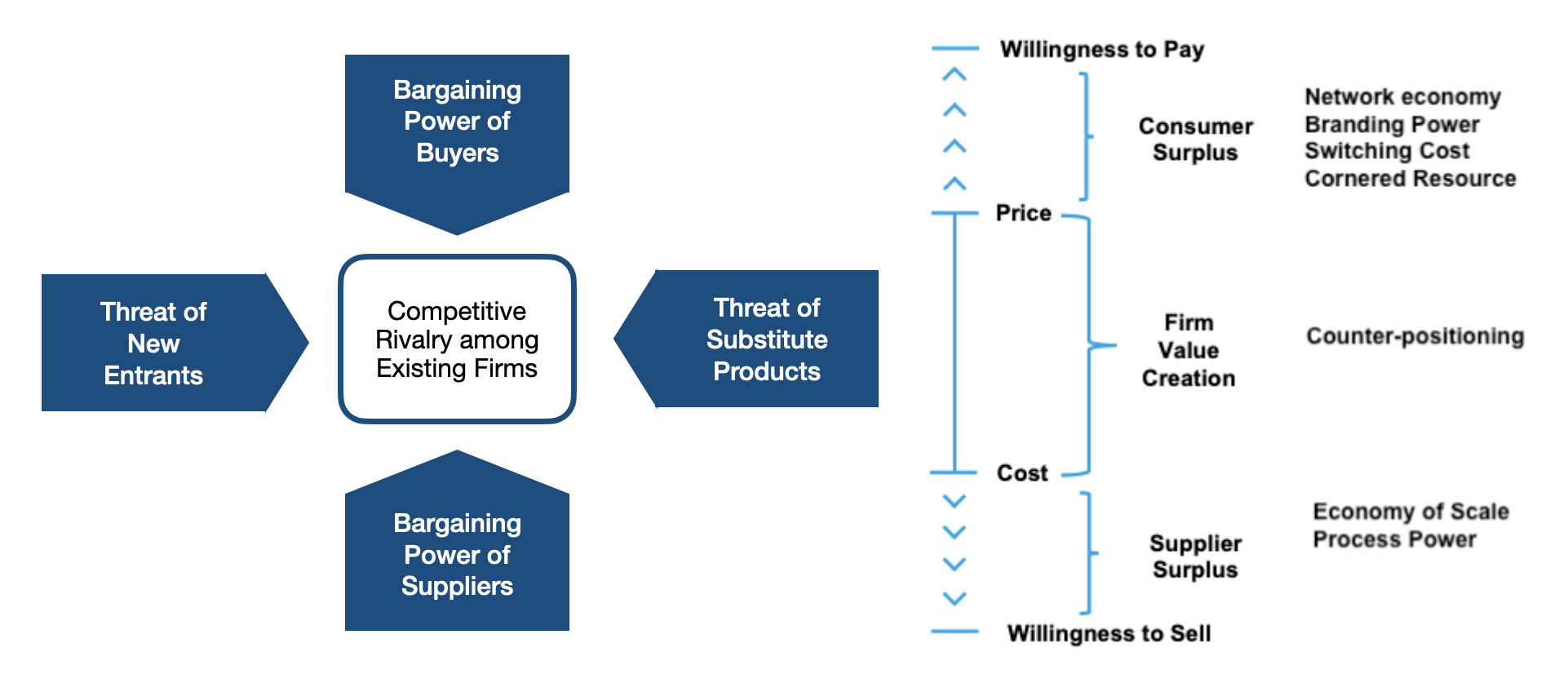

The SCP paradigm has since evolved into Porter’s Five Forces methodology (Porter, 2008) for analysing the competitive landscape and dynamics of an industry and the firms operating within it. The five forces, together with a statement of the associated risks and possible mitigations, are as follows.

- Rivalry Among Existing Firms — This refers to the behaviour and competitive intensity of existing players in an industry, to which a firm must respond in order to establish its own competitive advantage. Intense competition among existing firms in an industry can reduce overall profitability for all. In many industries, firms will act to avoid direct competition and promote legal cooperation. Examples of legal cooperation or coordination are synchronised price changes, done through signaling rather than explicit discussion, and restrained changes in industry capacity.

- Threat of New Entrants — The risk here is that new competitors will erode market share and profitability. To protect the industry and themselves, firms will act to establish strong barriers to entry through different means.

- Bargaining Power of Suppliers — Strong suppliers can increase input costs and squeeze firms’ profit margins. To mitigate this risk, firms will act to diversify their supplier base and also consider vertical integration.

- Bargaining Power of Buyers — This is related to the ability of customers to put a company under pressure by asking for more quality or demanding lower price. Strong buyers can force firms to become price-takers and limit their profitability. To address this risk, firms will act to differentiate their products and services and promote customer loyalty through different strategies.

- Threat of Substitutes — The risk here is that a firm’s product can be made irrelevant through substitutes that address the same consumer needs. Firms need to constantly innovate, improve products, and/or create switching costs in response.

In Porter’s analysis, the sequence of activities a firm performs to design, produce, sell, deliver, and support its products is called the value chain, which is part of a larger value system. These activities require a combination of human, intangible, and tangible capital. A company’s series of choices about its value proposition and its value chain is what gives rise to competitive advantage. From that perspective, strategic competition means choosing a path different from that of others in order to establish and sustain a difference from competitors, and competitive advantage manifests itself in simple quantifiable ways when delivering (differentiated) product: compared with rivals, you either operate at a lower cost, command a premium price, or both. One of Porter’s core message on competitive strategy is that instead of competing to be the best, companies can — and should — compete to be unique. In particular, competing to be the best feeds on imitation, but competing to be unique thrives on innovation. Strategic positioning is thus primarily about defining how a firm’s activities differ from those of the competition, and the five forces is a systematic way for a firm to understand the structure of an industry and how it should position itself within the industry to be competitive. And, of course, where there are differences, there are trade-offs and these trade-offs, in conjunction with path dependency and organisational inertial, are what make it possible for a competitive advantage to be entrenched.

Both SCP and the Five Forces Methodology has been further enhanced by modern takes like Helmer’s 7 Powers (Helmer, 2016) that describe active strategies that a company can pursue to enable it to “achieve persistent differential returns or to be more profitable than their competitors on a sustainable basis.” Such strategies are centered around

- exploiting scale economies and network economies to entrench one’s market position,

- maximising one’s branding power,

- introducing switching costs for customers,

- mastering complex processes as an application of learning curve theory,

- pursuing counter-positioning strategies that incumbents cannot easily respond to because of Innovator’s Dilemma (Christensen, 2015), and finally

- cornering an existing scarce resource.

To understand how these strategies can be used in practice, it can be helpful to overlay them on the so-called Value Stick (Oberholzer, 2021) as shown in Figure 2.

A firm creates value for itself by charging a price higher than its cost of delivering a product. The gap between the consumer’s willingness to pay for the product is the consumer surplus. Network economy, branding power, switching cost, and cornered resource are all powers that can be used to deliver more value, real or perceived, to a consumer than the price they are charged. This is sometimes referred to as a firm’s pricing power. The gap between the cost of delivering a product and the suppliers’ willingness to sell the required input raw materials, which includes workers and their time, to a firm (as opposed to its competitors) is the supplier surplus. Firms with strong economy of scale and/or process power have the ability to lower the cost to close to its suppliers’ willingness to sell. Finally, counter-positioning is a strategy a firm can use to compete with incumbents in an industry in a way that they cannot respond without disrupting their own business model.

It is worth noting that, in the analyses of both Porter and Helmer, strategies are there to deliver a firm sustainable superior profitability and, by definition, some immunity from competitive arbitrage like those envisioned in Adam Smith’s perfect-competition markets. Having said that, Exhibit 5 and Appendix A in (Mauboussin, 2024) show that most industries, as a whole, do not earn a sustainable return-on-invested-capital above the weighted-average-cost-of-capital, which suggest we do have good competitive dynamics a la Adam Smith in many parts of our economy. Obtaining competitive advantage is hard work; hard to achieve in the first place, and even harder to sustain over time.